One thing you look at when you check out your brokerage or 401k statement, is the rate of return of your investment decisions. This is calculated by taking the price appreciation and dividends earned on a stock, and dividing that total by the price you paid for the investment. This number is usually annualized.

As an example, take Coca-Cola (KO) stock. A year ago, from the time I am writing this, the stock traded at $46.09/share. Today, it sits are $54.33/share. The stock paid dividends equal to 3.01% in the past year. Now if you purchased Coca-Cola a year ago, the price of the stock has appreciated 17.88%. If you add the dividend yield, you have a return of 20.89%. Now we will focus on the cash-on-cash rate of return. Clearly, there are other factors to consider when purchasing investments; appreciation, tax benefits, and after tax income are a few.

The astute real estate investor will look at rates of return when considering investing in an income property compared to other alternative investments. Profit is made each year of ownership of an income property and realized at the time of sale. The annual income percentage is calculated by taking the cash flow after debt service (CFADS) and dividing it by the cash investment the investor made to purchase the property. As an example, if Joe Investor pays $3,675,000 for a net leased office building and receives $227,369 in CFADS, the cash-on-cash return is 6.2%.

If the investor borrows money, it reduces the amount of money they have to personally spend on the property. If the denominator is lower, than this should increase the rate of return, right? The correct answer here is maybe. Now we have all worked with borrowers who think the more money you can lend them, the higher their return will be. This may or may not be the case. It depends if the leverage environment is in a positive, neutral, or negative state.

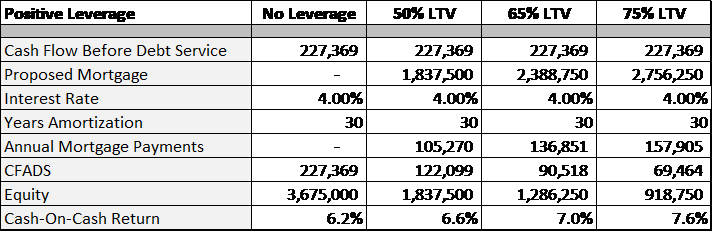

During most of the decade after the Great Recession, investment real estate in the United States was in a positive leverage environment. If you were to add more debt to the real estate purchase, the cash-on-cash return would increase. From an investor who is attempting to maximize their cash-on-cash return, borrowing more made sense. Doug Marshall, author of Mastering the Art of Commercial Real Estate Investing, outlined three good scenarios using the numbers above and exploring the three different states of leverage. First, consider the chart below for the impact of positive leverage.

Again, note how in this case, the cash return increases as the real estate investor puts less of his money into the property. This leads to the next scenario. Can it be possible that the amount of debt has no bearing on the cash return? The answer is yes. Consider this chart.

If you think that adding debt or adding equity can change the cash-on-cash return, there are possibilities where this is not so. Is there a possibility that the more debt is added, the lower the return will be? Consider the third chart

You will note the different factor in each of the three cases is the interest rate. For a portion of 2018, a negative leverage environment was present in commercial real estate, meaning the higher the property loan, the worse the cash-on-cash return will be. This situation curbed some astute investors’ appetite for borrowing on these real estate investments.

The environment changed from positive to negative with a significant rise in interest rates that was not followed by an increase in the cap rates. When interest rates rise, the higher mortgage payment reduces the property’s cash flow after debt service. Lower CFADS lowers the cash-on-cash return. To reduce this trend, the property value would need to drop or the cash flow before debt service would need to increase.

A protracted negative leverage environment may point to a correction in real estate prices. Other factors that may point to an drop in the real estate market could be increasing interest rates, moderating rental rate increases, excess real estate supply coming online, increasing vacancy rates, increasing rental concessions, or more regulation to restrict property owners. Recent decreases in interest rates have moved many U.S. markets back to a positive leverage environment. But if markets move back to the negative, buyers will pull back and may elect to pay capital gains and hold their money on the sideline instead of paying for overpriced properties.

Lenders, and astute investors, the cash-on-cash calculation should be made at an interest rate that is stressed higher than the initial rate on the credit, especially if the holding period for the real estate will exceed the first interest rate and payment change for the loan. Using an underwriting rate in the analysis is a sound judgement of the transaction’s ability to perform. Will the property be able to experience a higher cash flow before debt service to offset the higher mortgage payment and keep the return intact?

Now again, the cash-on-cash rate of return is only one tool to consider when looking at a real estate investment. It is important to understand this calculation and the part it will play in the buy or not buy decision.