Hospitality had an incredible year in 2018. The travel research firm STR reported U.S. hotel revenues at $218 billion, up $10 billion from 2017. This is an all time high. Profit also topped $80 billion. Occupancy and revenue per available room (RevPAR) have both grown each year in the past decade. Marcus & Millichap is predicting a 66.5% occupancy rate for 2019, which would be a 30-year record high.

The questions are what has caused the bull market for hotels in the first place and how long can this last?

Skyler Cooper, director of Marcus & Millichap’s National Hospitality Group, cites the extended period of U.S. job growth with higher earnings, economic expansion and consumer confidence all have led to higher leisure and business travel. The industry has also benefitted from an increase of foreign investment, with 12.3% of new hotels being funded by sources outside the U.S. The highest proportion of foreign investments land in New York, Miami, and San Diego.

Large cities such as New York, San Francisco, Los Angeles, San Diego, Orange County, Boston, Miami, and Orlando have the highest occupancy rates. Investment in these areas is often faced with high barriers to entry, less land that is available to build, high labor costs, more bureaucratic red tape, and longer construction time periods. As a result of these challenges, secondary and tertiary markets with less hurdles to overcome are becoming popular, but even those areas are becoming crowded. Cites like Austin, Texas, Nashville, Chicago, Seattle, and Detroit are all seeing substantial new supply.

A lot of markets which have not had a good supply of hotels to support leisure demand in the past now are popping up with small hotels. But this is not certain to get heads in beds if it is built. There needs to be solid core demand generators and good supplement of leisure travelers. One hotel I worked with in Denver had a very strong Sunday to Thursday crowd. Their location to several sporting venues made anything on the weekend a bonus when the professional teams were in town. But the business traveler made the bulk of the stable revenue stream.

Hotels seem to be on the leading edge of economic activity. If the economy slows down, travel slows down. More businesses will move away from the personal trip and opt for video conferencing (which will be more of a factor as technology progresses). Individuals who may feel less real wage growth may delay some trips or select a less expensive alternative. These trends tend to be on the front end of any economic trend, so any economic slowing will hit hospitality early.

Another headwind is the increasing labor cost and shrinking labor pool of possible workers in the industry. One of the largest costs for a hotel could be housekeeping, desk, management, and sales staff. Not only is there the increased cost to pay help, but there is also the high cost if you end up selecting the wrong employees.

Costs for building new hotels has been increasing. Some material costs are up with the new trade tensions and tariffs. Construction costs on the labor side are edging up. Contractors are seeing strong demand from apartments and mixed-use real estate. The hotel developer is competing against strong demand in other real estate classes.

Hotel rooms are also facing competition for room rentals from VRBO and Airbnb. A few years ago, there was more panic in the industry with these competitors. In some areas, the short-term rental market could capture 10-15% of room demand. But now, the concern has subsided somewhat. These players have been in the market for a few years and yet the hotel room rates and occupancy continue to climb. Some municipalities are passing laws to level the playing field between a hotel and short-term rental.

Hotel developers should look at more factors than just the occupancy and RevPAR. The growth rate of room rates, level of new supply, population growth, labor supply, employment growth, and infrastructure investment are all factors that should be considered. Changes in demand should be inspected to see if this is limited to a certain brand, service level, chain, or even an event.

Lenders are still looking at hotels, but the appetite is less than it was a few years ago. Some are staying on the sidelines completely. Others are complaining they are not seeing deals that are good enough currently. It is hard to see the upside of a new hotel when you have high occupancy levels and not a lot of rate growth. Increases in operating expenses, like labor, will have a downward pressure on operating profits. Stress testing the historical or projected income stream is essential. Having management that can identify any negative changes in the market and adjust quickly to bolster net operating income is important for the hotel to succeed.

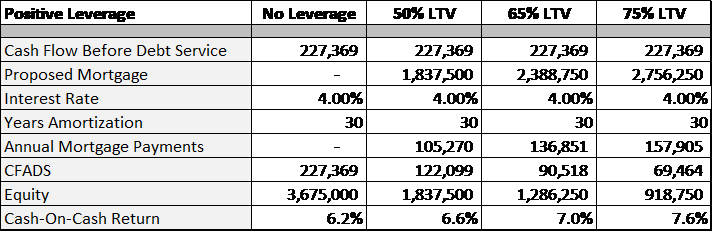

Leverage rates should be lower on these properties. Since there is a fairly high cost of basic operations just to keep the doors open, high debt service requirements will kill a hotel. Perhaps the ones which make it in the end are the ones who can put the extra 5-10% into the project.