In my last blog, I identified several structural items necessary for a lending institution to identify and manage problem credits. This blog will point out several factors that may indicate problems with your corporate borrower. Like a good bloodhound, you must be able to sniff each of these and determine when there is a problem involved that will impact your ability to be repaid.

New Borrowings from Other Creditors may be a clue of problems. I once had a car dealer who said he believed in spreading business around town with loans at several institutions. Over the period of a couple of years, he added five new lenders who advanced funds for real estate, equipment, inventory, and working capital. When the business imploded, no lender had adequate knowledge of the business and control of the lending to enforce their position, so we all were comrades in misery as we took losses across the board.

New credit that pops up is especially problematic when it is a surprise to the lender. Often, we have seen this in ag lending when a new filing by John Deere pops up on a UCC search when the operating lender had no knowledge of any planned capital purchases. It is really a problem if you have a “no new borrowing without lender approval” covenant which is violated.

A new loan made by someone else when you turned down the request because of financial issues with the company may be a sign. On some of the marginal companies we bank, we often hope there will be a greater fool out there who will close the next credit for them. This is a real problem if the greater fool does not pay off the existing debt with us in the process.

Tax Liens may signal a problem. This can come in many forms: property taxes, sales taxes, income taxes, withholding taxes, to name a few. Of these, a failure to pay withholding taxes to the IRS is very egregious since most of these funds come from the employee. Missing any required taxes is a sign of cash flow problems in the company and must be addressed. Also, tax liens of the business owners may show the company is not producing enough cash to provide distributions to the owners to pay for their tax liability from tax profits generated by the company.

Delinquency and Overdrawn Deposit Accounts are obvious signs of cash flow problems. Unfortunately, these are often signs that occur very late in the problem cycle and may indicate problem issues are exacerbating. Now these may be caused by poor loan structuring, and in those cases, the lender may be able to help solve the problem with a proper structure. We had a loan on a seasonal hotel which had problems making payments in the off-season, especially close to the time toward the end of the off-season when expenses to reopen the hotel were high. This was solved simply by a seasonal payment structure that matched the business cash flow.

Concentrations of Business may indicate a serious problem in a business. This can come from over-reliance on one customer in terms of sales or receivables. I once worked with a horizontal contractor who had a large multi-year contract in a large subdivision. The developer overextended himself and sales stalled. Consequently, the contractor suffered a large loss which took several years to recover from. Another case I know comes from a manufacturer of perfumes who had their main account, over 75% of their sales, to Wal Mart. When Wal Mart found a cheaper source of product, the business scrambled to downsize because of the lost business. In each of these cases, greater diversification could have staved off some cash flow issues.

Violation of Loan Covenants may be a strong indication of a foul smell coming from your borrower. This is assuming that you have well-structured loan covenants in place to begin with. Covenants are like good medical equipment to check the overall health of the company. The lender needs to identify when one is broken, what caused the problem, and what possible solutions may be. You should also look at the negative side to see what future problems may occur if the covenant remains broken or the company’s performance weakens further.

Expansion may be a problem, especially if it is completed too rapidly or made in an unrelated business line or market area. Bigger does not always mean better, it just means bigger. Many companies have failed as a result of growing quicker than their ability to service that growth. Also, large spikes in revenues may present a problem when income drops. We saw this recently with grain prices when farmers became comfortable with high prices earlier in this decade and began to make purchase decisions based upon those prices continuing into the foreseeable future. Growth into a new market may not present the same revenues and net profit as the company experienced in the current establishments.

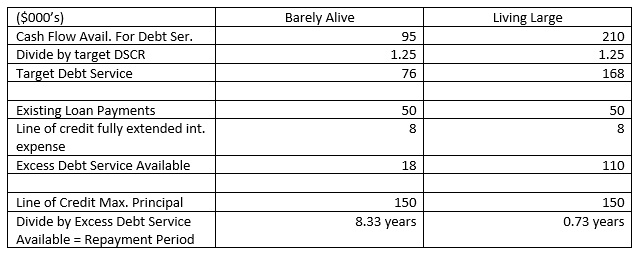

Failure to Pay Off Lines of Credit will show cash flow issues in the company. In agricultural lending, we refer this as carry-over debt, or a short-term line of credit that the producer failed to generate sufficient revenues to retire. Any operating line of credit that cannot be retired in an operating cycle must be sniffed out to see the cause. Did the company use it for purchasing fixed assets? Is there a deterioration of business that is causing the company cash flow problems? Often this may give the lender one of the early whiffs of foul credit.

Withholding Information is a huge sign that something is rotten with your borrower. This is often the worst position a lender can be in, not knowing what they do not know. Have you ever had a borrower who refused to answer detailed questions we had regarding their finances? If you do, this may be the sign that something rotten is being covered up.

Change may be a sign that something is smelly in your credit. The change may be in the accountant, bookkeeper, management, leadership, industry, environment, or other factors. Sometimes, these changes may signal a problem. The lender should consider if any of these issues should require the loan to be watched more closely to see if what you smell is passing or is an indication of rottenness.

These are some factors that the credit bloodhound must sniff through as they manage their portfolio. Identification of the problem is the first step in proper credit management.